Arrears in 4-FSS: how not to get confused in terms

We do not have an official definition of the concept of “arrears in 4-FSS” in the legislation. The term “arrears” is disclosed in Art. 11 of the Tax Code of the Russian Federation and means the amount of tax, fee or insurance premiums not paid within the period established by law.

The arrears that policyholders reflect in 4-FSS do not relate to tax payments. Although it means the same thing - this is the amount of outstanding contributions for which the payment deadline has expired. In this case we are talking about insurance premiums “for injuries”, which are administered by the Social Insurance Fund.

Two concepts should be distinguished:

- “debt owed by the policyholder at the end of the reporting (settlement) period” is a normal phenomenon when the policyholder has accrued contributions due on the reporting date (for the last month), and the payment deadline for them has not yet arrived (will occur in the next month, which belongs to another reporting period);

- “arrears” - its presence indicates that the policyholder has delayed payment of premiums and will be financially punished for this (see below for the consequences of arrears).

To avoid arrears in contributions for injuries, the policyholder should monitor the timeliness of payment of contributions - monthly no later than the 15th day of the calendar month following the month for which contributions are calculated (Clause 4 of Article 22 of the Law “On Compulsory Social Insurance...” dated July 24, 1998 No. 125-FZ).

We tell you what the differences are between penalties, fines and penalties.

WHERE to submit the report, DEADLINES and METHODS FOR SUBMISSION 4-FSS

Where to submit the payment

If the organization does not have separate divisions, then submit the calculation to the territorial office of the Social Insurance Fund at its location (clause 1 of Article 24 of the Law of July 24, 1998). That is, at the place of registration of the organization.

If the organization has separate divisions, then Form 4-FSS must be submitted in the following order. Submit the calculation to the territorial office of the FSS at the location of the separate unit only if:

- such a unit has a current (personal) account

- and independently pays salaries to employees.

Note: In this case, in the 4-FSS form, indicate the address and checkpoint of the separate unit.

When the above conditions or at least one of them are not met, include all indicators for such a division in the calculation for the head office of the organization and submit it to its location. Do the same if the separate division is located abroad. This follows from the provisions of paragraphs 11, 14 of Article 22.1 of the Law of July 24, 1998 No. 125-FZ.

to menu

Calculations in Form 4-FSS must be submitted at the end of each reporting period.

There are four such periods: the first quarter, half a year, nine months and a year:

- They must be submitted on paper no later than the 20th

- In electronic form - no later than the 25th day of the month following the reporting period.

If the deadline for submitting a calculation falls on a weekend, report on the next business day. This follows from the Civil Code of the Russian Federation. Although the rule on rescheduling is not directly stated in Law No. 125-FZ of July 24, 1998, other areas of legislation can be applied by analogy.

Kontur.Extern: How to easily submit a new 4-FSS form through an EDF operator

to menu

Special line for arrears

How to reflect arrears in 4-FSS? You need to show the arrears in 4-FSS on line 20 - this is the final line in Table 2 “Calculation of compulsory social insurance against industrial accidents and occupational diseases”:

Line 20 details line 19 “Debt owed by the policyholder at the end of the reporting (settlement) period” in terms of the amount of arrears. It shows for reference how much of the total debt amount is arrears.

Find out about important tax innovations for 2021:

- “Increasing the amount of the tax deduction for children from 2020”;

- “What changes await PSN from 2021: nuances”;

- “Changes in accounting statements from 2021”;

- “Bad debts of individuals can be written off without personal income tax.”

Fake sick leave certificates

Sometimes unscrupulous employees pretend to be sick so as not to come to work. And they even bring a sick leave certificate as confirmation. This way they can take a few extra paid days off.

In addition, it is now possible to obtain sick leave without going through a doctor or clinic. There are a lot of advertisements on the Internet in which, for a small amount, they offer to issue a certificate of incapacity for work, even retroactively. Perhaps, at first glance, such a sick leave will be no different from the real one. But fund inspectors will definitely not miss a fake document. And, of course, they will not reimburse benefits for it.

As a result, the company will have arrears in insurance contributions to the Pension Fund and the Social Insurance Fund. After all, there is no need to pay contributions for sick leave benefits. But it is mandatory for all other payments in favor of the employee. Including the amount that the employee received in the form of sick leave.

If you have doubts about the sick leave certificate, check its authenticity as follows:

- On the FSS website, in the “Employers” section, the list of stolen sick leave forms is updated monthly (). Check the questionable document number against this list.

- Call the clinic that issued the sick leave and ask if they issued a document with that number. If yes, then it should be in the medical institution’s database. It is advisable to obtain written confirmation from a doctor.

- Write a request to the FSS in free form with a request to establish the authenticity of the sick leave. In the letter, provide the details or attach a copy of the certificate of incapacity for work.

Also, explain to employees in advance that buying fake sick leave is a criminal offense. Liability is provided for under Part 3 of Art. 327 of the Criminal Code - use of a deliberately forged document. Not to mention the dismissal for absenteeism and the collection of benefits from his salary.

Determining the indicator for line 20

There is no legally established algorithm by which the amount of arrears can be calculated to reflect it in line 20 of the 4-FSS report. We will not find the necessary formulas or descriptions in the Procedure for filling out 4-FSS, approved. by order of the FSS of the Russian Federation dated September 26, 2016 No. 381.

However, line 20 of form 4-FSS, if the policyholder has arrears, must be filled out, like the rest of the indicators in table 2. Order No. 381 indicates only the general direction of data search - table 2 is filled out based on the policyholder’s accounting records.

The arrears take into account all late payments, except for the late payment for the last month. So, to calculate the amount of arrears, you should add up everything that has not been paid as of the reporting date, without taking into account the last calendar month - the contributions accrued for this month are considered simply arrears until their payment is due.

Example 1

The accountant of Ritm LLC, when filling out the 4-FSS for the 1st quarter of 2020, on line 19 of Table 2, indicated the insured's debt at the end of the period - 28,644 rubles. At the same time, the amount of contributions accrued for March 2021, based on the report data, amounted to 19,172 rubles.

Considering that the deadline for payment of contributions for March falls on 04/15/2020, the amount of contributions accrued for March (RUB 19,172) will be ordinary debt. And the remaining amount is 9,472 rubles. (28,644 - 19,172) - arrears. It should be indicated on line 20 of Table 2.

Let's change the conditions of example 1 and show how to fill out line 20 if the policyholder has no arrears:

Example 2

According to the accounting data of Rhythm LLC, the company’s debt on contributions for injuries at the end of the 1st quarter of 2021 amounted to 19,172 rubles. — this amount of contributions was accrued for March 2021. Ritm LLC plans to pay this amount no later than 04/15/2020.

Considering that the company has no other debts on contributions for injuries, the accountant, when filling out 4-FSS, will reflect:

- on line 19 (debt of the policyholder at the end of the reporting period) - 19,172 rubles;

- on line 20 (including arrears) - a dash (19,172 - 19,172 = 0).

If there is a dash in line 20, the policyholder should not worry.

Answer

We inform you the following: No, you cannot. The procedure for filling out Form 4-FSS, approved by the Ministry of Labor No. 107n dated March 19, 2013, does not provide for the reflection of accrued penalties in Table 7.

The rationale for this position is given below in the materials of the Glavbukh System

Order of the Ministry of Labor of the Russian Federation dated March 19, 2013 No. 107n “On approval of the form of calculation for accrued and paid insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity and for compulsory social insurance against industrial accidents and occupational diseases, as well as expenses for payment of insurance coverage and the Procedure for filling it out (as amended as of February 11, 2014)"

Appendix No. 2

30. The table is filled out based on the policyholder’s accounting records.

31. When filling out the table:

31.1. line 1 reflects the balance of the account credit for settlements with the Fund for compulsory social insurance against industrial accidents and occupational diseases. This indicator does not change during the billing period;

31.2. line 2 reflects the amount of accrued insurance contributions for compulsory social insurance against accidents at work and occupational diseases from the beginning of the billing period in accordance with the amount of the established insurance tariff, taking into account the discount (surcharge). The amount is divided “at the beginning of the reporting period” and “for the last three months of the reporting period”;

31.3. line 3 reflects the amount of contributions accrued by the territorial body of the Fund based on on-site inspection reports;

31.4. line 4 reflects the amounts of expenses not accepted for offset by the territorial body of the Fund for past billing periods based on reports of on-site and desk inspections;

31.5. line 5 reflects the amount of premiums accrued for previous years both by the policyholder himself and based on the results of a desk audit;

31.6. line 6 reflects the amounts received from the territorial body of the Fund to the bank account of the policyholder in order to reimburse expenses exceeding the amount of accrued insurance premiums;

31.7. line 7 reflects the amounts transferred by the territorial body of the Fund to the bank account of the policyholder as a refund of overpaid (collected) amounts of insurance premiums;

31.8. line 8 “Total (sum of lines 1+2+3+4+5+6+7)” – control line, which indicates the sum of the values of lines 1 to 7;

31.9. line 9 reflects the amount of debt owed to the territorial body of the Fund at the end of the reporting period (debit balance of the account on which calculations are made for compulsory social insurance against industrial accidents and occupational diseases);

31.10. line 10 reflects the debit balance of the account for settlements with the Fund for compulsory social insurance against industrial accidents and occupational diseases (based on the policyholder’s accounting data). This indicator does not change during the billing period;

31.11. line 11 reflects the costs of compulsory social insurance against industrial accidents and occupational diseases on an accrual basis from the beginning of the year, broken down “at the beginning of the reporting period” and “for the last three months of the reporting period”;

31.12. line 12 reflects the amounts transferred by the policyholder to the bank account of the territorial body of the Fund, cumulatively from the beginning of the year, broken down “at the beginning of the reporting period” and “for the last three months of the reporting period” indicating the date and number of payment orders;

31.13. line 13 reflects the written off amount of the insured's debt in accordance with the regulatory legal acts of the Russian Federation adopted in relation to specific policyholders or the industry for writing off arrears;

31.14. line 14 “Total (sum of lines 10+11+12+13)” – control line, which shows the sum of the values of lines 10 to 13;

31.15. line 15 shows the balance of debt owed to the policyholder at the end of the reporting period (credit balance on the account on which payments are made for compulsory social insurance against accidents at work and occupational diseases), including line 16 shows the amount of overdue debt calculated by the policyholder himself based on accounting data."

The debt of the policyholder, be it an entrepreneur or a law firm, is the difference in the amounts of accrued and paid premiums according to government officials. But how is this value formed and is it possible to influence and control it? Agree, it’s unpleasant if you decide to participate in the auction, and they give you a certificate that you are a debtor under the Social Insurance Fund, so you can lose an excellent client. To avoid getting into such an unpleasant situation, you need to:

- submit reports to the Social Insurance Fund on time

- carefully fill out all the cells of the report

- pay dues on time

- correctly indicate KBK in payments

- periodically check with the fund

The composition of arrears of contributions includes:

- balance of debt at the beginning of the period

- “+” amount of accruals for the reporting period

- “-” the amount of transfers of insurance premiums with the correct details

This is how we get the total amount of arrears on contributions.

Why is arrears dangerous?

Arrears are always punishable. It is not for nothing that its amount needs to be shown for reference in line 20 of Table 2 of the 4-FSS report - the appearance of any figure in this line signals that the policyholder has an overdue debt to the Social Insurance Fund and measures must be taken to repay it as quickly as possible.

For example, the presence of arrears is the reason for receiving a refusal from the Social Insurance Fund to provide financial support for preventive measures to reduce industrial injuries and occupational diseases of workers:

Another negative factor in the presence of arrears is the accrual of penalties on its amount. And these are unplanned additional expenses for the policyholder. The FSS is responsible for calculating penalties according to the following rules:

If you do not pay the arrears of contributions for injuries and penalties on time, the FSS will forcibly collect the amounts from the insured’s account or at the expense of his property.

VIDEO: New 4-FSS, What changes to take into account in the report, starting with reporting for the nine months of 2017

Watch video on youtube.com

Program:

- What has changed in the 4-FSS calculation form for nine months. New clarifications from the Social Insurance Fund and other departments on contributions for injuries

- Recent clarifications from the Social Insurance Fund, which are important to take into account when reflecting payments to employees, change of position.

- How not to make a mistake with OKVED in a report: how to determine and where to check. Dependence of tariffs on OKVED, filling out table 1.

- What to consider when filling out the line “Average number of employees”: how not to make a mistake in calculating the indicator.

- Who should sign the report to the Social Insurance Fund now? Requirements for electronic signature. Power of attorney.

- Features of filling out table 1.1.

- What debts to the Social Insurance Fund and overpayments to the fund should be reflected in Table 2. What dates should the data be limited to: upon payment, upon accrual.

- Features of filling out tables 3 and 4.

- How to claim expenses for improving working conditions. What activities does the Social Insurance Fund finance and how to reimburse it.

- What to consider when reflecting data on the special assessment of working conditions.

- Errors in 4-FSS. Control ratios for checking the report

- Contribution rate for injuries

- Average number of employees for 4-FSS

- How to submit and sign a 4-FSS calculation. Errors when sending electronic reports

- How to fill out special 4-FSS tables

- How does the Social Insurance Fund finance activities to reduce injuries?

- Information about special assessments and medical examinations. Calculation table 5

- Responsibility for non-payment of contributions for injuries and delays with 4-FSS

- Rounding in 4-FSS. Tips for accountants

to menu

Results

Arrears are the amounts of contributions not paid on time. In 4-FSS, arrears in contributions for injuries are reflected for information in line 20 of Table 2. If the insured has an arrear, penalties are charged for its amount. In addition, the Social Insurance Fund may refuse to provide financial support for preventive measures to reduce industrial injuries and occupational diseases of workers.

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

General information about the organization

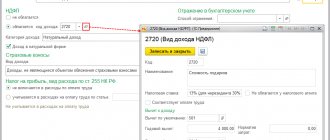

To correctly fill out the calculation for the organization, the following must be indicated: full name, in accordance with the constituent documents, TIN, KPP, OGRN, OKVED codes, registration number of the policyholder, subordination code, registration address and information about the head of the organization. The necessary information is indicated in the Organizations directory (section Settings - Organizations) (Fig. 1).

Rice. 1

Information about the tariff of insurance premiums

The rate of contribution for compulsory social insurance against accidents and occupational diseases is established for the policyholder for each year by the territorial body of the Federal Social Insurance Fund of the Russian Federation, depending on the class of professional risk of the type of activity carried out by the policyholder. The established tariff rate is entered in the Contribution rate to the Social Insurance Fund NS and PZ field, indicating the start date of its application in the organization’s accounting policy settings form (section Settings - Organizations - Accounting policy and other settings tab - Accounting policy link - Insurance premiums tab). Moreover, the rate is indicated taking into account the discount/surcharge (if it is established for the policyholder), i.e. the resulting rate at which insurance premiums should be calculated. For more information on filling out the form, see the article Information on insurance premium rates.

Rice. 2

Accounting for income for the purposes of calculating insurance premiums

For the correct accounting of income received by individuals for the purposes of calculating insurance premiums and for further filling out the indicators for calculating the base for calculating insurance premiums in the calculation, it is also recommended to check and, if necessary, clarify the settings of the types of accruals with which the program makes accruals to employees for worked and unworked time. All payments and other rewards in favor of individuals in the program are calculated using accrual types (section Settings - Accruals). For each type of accrual, on the Taxes, contributions, accounting tab, in the Insurance premiums section, the type of income must be indicated for the purposes of calculating insurance premiums (Fig. 3). For more information about this, see the article Setting up the imposition of insurance premiums on various types of charges.

When posting documents with the help of which accruals are made in favor of individuals (for example, documents Calculation of salaries and contributions, Bonuses, Financial assistance, Dismissal), the corresponding type of income is recorded for the purposes of calculating insurance premiums. This data is used to determine the basis for calculating insurance premiums and filling out Table 1 of the calculation. You can obtain data on the formation of the base for calculating insurance premiums using the report Analysis of contributions to funds (section Taxes and contributions - Reports on taxes and contributions - Analysis of contributions to funds - version of the Social Insurance Fund report (accidents, occupational diseases).

Rice. 3

Remunerations under GPC agreements are subject to insurance contributions for compulsory social insurance against industrial accidents and occupational diseases only if this obligation is provided for in the agreement (paragraph 4, paragraph 1, article 5 of the Federal Law of July 24, 1998 No. 125-FZ) . If such an obligation is provided for in the contract, then in the Contract (work, services) document, check the Subject to accident insurance checkbox (Fig. 4). In this case, the remuneration will be subject to contributions to compulsory health insurance, compulsory medical insurance and to the Social Insurance Fund for NS and PZ, in addition to compulsory social insurance in case of temporary disability and in connection with maternity.

Rice. 4

In addition, the program can register other income received by individuals from the organization. For such income, the following is indicated for calculating insurance premiums:

- when registering payments to former employees - in the Types of Payments to Former Employees directory;

- when registering other income of individuals - in the directory Types of other income of individuals;

- when registering copyright agreements with individuals - in the Types of Copyright Agreements directory;

- when registering prizes, gifts from employees - if insurance premiums need to be calculated on the cost of the gift, then in the Prize, gift document, check the Gift (prize) is provided for by the collective agreement checkbox.

Calculation of insurance premiums

Insurance contributions for compulsory social insurance against accidents and occupational diseases are calculated separately for each individual. The legislation does not provide for a maximum base for these contributions.

The calculation of insurance premiums in the program is carried out using the document Calculation of salaries and contributions when completing the procedure for filling out a document or other document by which contributions are calculated (Dismissal, Parental Leave). The amounts of accrued insurance premiums for each individual are reflected on the Contributions tab of the document Accrual of salaries and contributions (Fig. 5). When posting the document, the amounts of accrued contributions are recorded. Based on these data, the calculation fills in information about the amounts of accrued insurance premiums in Table 2. You can obtain data for analyzing the amounts of accrued insurance premiums using the Analysis of Fund Contributions report. You can check the correctness of the calculation of insurance premiums for a certain period using the report Checking the calculation of contributions (section Taxes and contributions - Reports on taxes and contributions - Checking the calculation of contributions - FSS_TS report option). For more information on the calculation of insurance premiums, see the article Calculation of insurance premiums.

Rice. 5

Calculation of contributions from payments in favor of disabled people

If the organization employs disabled people of groups I, II or III, in respect of whose payments insurance premiums for insurance against accidents and occupational diseases are paid in the amount of 60% of the insurance rate (clause 2 of article 2 of the Federal Law of December 22, 2005 No. 179- Federal Law), then it is necessary to fill out information about disability (Fig. 6). In the calculation using Form 4-FSS, the amount of accruals in favor of disabled individuals is shown separately in column 4 of Table 1. Also on the title page of the calculation, the number of working disabled people is automatically calculated. For more information about the calculation of insurance premiums from payments in favor of disabled people, see the article Insurance premiums from payments in favor of disabled people.

Rice. 6

Calculation of contributions from payments in favor of foreigners

Contributions for compulsory insurance against industrial accidents and occupational diseases are paid for all foreign citizens, regardless of their status (Clause 2, Article 5 of Federal Law No. 125-FZ of July 24, 1998). Article 20.2 of Federal Law No. 125-FZ of July 24, 1998 does not provide for an exemption from insurance premiums for payments in favor of foreign employees.

Insurance Cost Data

Using funds from compulsory social insurance against accidents and occupational diseases, employers pay to insured persons who are in an employment relationship with them, security for this insurance in the form of:

- temporary disability benefits awarded in connection with an industrial accident;

- temporary disability benefits due to occupational diseases;

- payment for vacation for sanatorium treatment (in addition to annual paid leave) for the entire period of treatment and travel to and from the place of treatment.

Expenses for this type of social insurance made by the employer are counted towards the payment of insurance premiums for insurance against accidents and occupational diseases.

Payment of other types of insurance coverage (in the form of one-time and monthly insurance payments, payment of additional expenses related to medical, social and professional rehabilitation), provided for by Federal Law No. 125-FZ, is made to the insured person by the insurer, i.e. FSS of the Russian Federation (clause 7, article 15 of Federal Law No. 125-FZ).

Benefits for temporary disability due to an industrial accident or occupational disease are registered in the program using the Sick Leave document. Payment for vacation for the period of sanatorium-resort treatment - with the Vacation document. Data on accrued benefits and vacation are used when filling out table 3 of the calculation. You can obtain data on accrued benefits and leave for the period of sanatorium-resort treatment using the report Register of benefits at the expense of the Social Insurance Fund (section Taxes and contributions - Reports on taxes and contributions - Register of benefits at the expense of the Social Insurance Fund).

Information about paid insurance premiums

Policyholders are required to pay mandatory payments for insurance premiums no later than the 15th day of the calendar month following the calendar month for which the monthly mandatory payment for insurance premiums is calculated. If the specified deadline for payment of the monthly obligatory payment falls on a day recognized in accordance with the legislation of the Russian Federation as a weekend and (or) a non-working holiday, the expiration date of the deadline is considered to be the next working day following it (Clause 4 of Article 22 of Federal Law No. 125-FZ ).

The amount of insurance premiums to be transferred to the Social Insurance Fund of the Russian Federation is determined in rubles and kopecks (without rounding) (Clause 5, Article 22 of Federal Law No. 125-FZ).

The fact of payment of insurance premiums in the program is reflected using the document Payment of insurance contributions to funds (section Taxes and contributions - Payment of insurance contributions to funds) (Fig. 7). Indicators of paid contributions are reflected in table 2 of the calculation. Payment of contributions accrued according to inspection reports is also recorded in the document Payment of insurance contributions to funds.

Rice. 7

<<- return to the beginning of the article

The procedure for filling out Form 4 FSS with an example and explanations

The rules for preparing a declaration of contribution for “injuries” are prescribed in the Procedure approved by Order No. 381 of the Federal Social Insurance Fund of Russia dated September 26, 2021. In many ways, they coincide with the rules for tax reporting. When calculating using Form 4-FSS, be sure to fill out the title page, tables 1, 2 and 5. The remaining tables - only if there is data that needs to be reflected. These are the requirements of paragraph 2 of the Procedure, approved by Order No. 381 of the FSS of Russia dated September 26, 2021.

When filling out the Calculation form, only one indicator is entered in each line and the corresponding columns. If there are no indicators provided for in the Calculation form, a dash is placed in the line and the corresponding column.

Average number of employees in 4-FSS

The adjusted calculation is made according to the form that was in effect during the period for which you identified errors. Please indicate the updated calculation number on the title page in the “Adjustment number” field. For example, if you have clarified the calculation for the second quarter of 2021 for the first time, enter the number 001.

If there is arrears, then first transfer the remaining contributions and penalties to the fund. Then you will not be charged a fine (subclause 1, clause 1.4, article 24 of Law No. 125-FZ of July 24, 1998).

Note: Please submit updated calculations in Form 4-FSS for periods before January 1, 2021 to FSS branches (Article 23 of Law No. 250-FZ dated 07/03/2016). It doesn’t matter that they include information not only about contributions for injuries, but also about contributions for compulsory social insurance. For more information, see How to make changes to insurance premium calculations (ERSV).

The organization is obliged to recalculate and pay additional contributions if the fund has increased the tariff due to a change in the main type of activity. At the same time, when the organization receives a notification about the tariff change, then, most likely, the 4-FSS calculation for the first quarter will already be submitted. It is not necessary to clarify its organization - the recalculation of contributions is not due to an error, but to the fact that the fund has established a new tariff. However, territorial branches of the Social Insurance Fund in some regions require clarification of the calculation for the first quarter. Therefore, find out the position of the fund at the place of registration of the organization.

Recalculation of contributions at the new tariff due to a change in the main type of activity is shown in table 2 of the calculation for the half-year:

- on line 5 “Contributions accrued by the policyholder for past billing periods” - the amount of contributions to be paid additionally;

- line 16 “Insurance premiums paid” – details of the payment order and the amount, if you have already paid the recalculated premiums;

- line 19 “Debt owed by the policyholder at the end of the reporting (calculation) period” - the recalculation amount, if additional contributions have not yet been paid.

In line 2 “Accrued for payment of insurance premiums” do not enter the recalculation, otherwise the control ratios will not converge. The indicator “at the beginning of the reporting period” in line 2 of table 2 of the report for the half-year should be equal to the accrued contributions from column 3 of line 2 of table 2 of the report for the first quarter (FSS order No. 83 dated 03/09/2017). Also, the unpaid recount is not a debt, so do not enter it on line 20.

The Social Insurance Fund can reduce the rate of contributions “for injuries” if the organization has . Recalculate contributions at the new rate from the beginning of the calendar year. The overpayment can be returned or offset against future payments (Article 26.12 of the Law of July 24, 1998 No. 125-FZ). In this case, it is safer to submit an update using Form 4-FSS.

There are no special lines in the calculation where you can indicate how you recalculated the contributions. The fund's auditors simply will not understand where the overpayment came from. Don't forget to change the fee rate to the current one. You indicate it in lines 5 and 9 of Table 1 of the calculation. In table 2 clarifications for the first quarter, indicate:

- on line 2 “Accrued for payment of insurance premiums” - accruals recalculated at a reduced rate;

- lines 9 “Debt owed by the territorial body of the Fund at the end of the reporting (calculation) period” and 11 “Due to overpayment of insurance premiums” - the amount of overpayment that the organization incurred;

- line 16 “Insurance premiums paid” – the actual amounts of premiums transferred.

Data for an example of filling out 4-FSS for 9 months of 2021.

Below are the initial data for an example of how to fill out form 4-FSS if the organization uses the labor of disabled people.

The organization employs one group II disabled person. Contributions for insurance against accidents and occupational diseases are calculated:

- at a rate of 0.2 percent (1st class of professional risk according to the Classification of Economic Activities by Class of Professional Risk) - from payments to all personnel, except for disabled people;

- at a rate of 0.12 percent (0.2 × 60%) - from payments to a disabled person.

As of January 1, 2021, the organization had a debt to the Federal Social Insurance Fund of Russia for contributions to insurance against accidents and occupational diseases for December 2021 in the amount of 290 rubles. During the reporting period, contributions for insurance against accidents and occupational diseases are listed in the following amounts:

- in January – 290 rubles. (fees paid on January 12 – for December 2016);

- in February - 76 rubles. (fees paid on February 12 – for January 2017);

- in March – 76 rubles. (fees paid on March 14 – for February 2017);

- in April – 76 rubles. (fees paid on April 13 – for March 2017);

- in May – 86 rubles. (fees paid on May 12 – for April 2017);

- in June – 86 rubles. (contributions paid on June 14 – for May 2017);

- in July – 86 rubles. (fees paid on July 12 – for June 2017);

- in August – 86 rubles. (fees paid on August 14 – for July 2017);

- in September - 86 rubles. (fees paid on September 12 – for August 2017).

Contributions for September 2021 in the amount of 86 rubles. were listed in October 2021, that is, outside the reporting period.

The accountant reflected the status of settlements with the Federal Social Insurance Fund of Russia for contributions to insurance against accidents and occupational diseases, the calculation base and the amount of accrued insurance premiums in form 4-FSS for the 9 months of 2021. There were no industrial accidents in the organization. Activities to prevent injuries and occupational diseases were not funded. Therefore, the accountant did not fill out tables 3 and 4 of form 4-FSS.

During 2021, the policyholder will assess working conditions. The accountant entered its results into Table 5.

to menu

Arrears on insurance contributions to the Social Insurance Fund

Update: February 15, 2021

Starting from 2021, the payment of insurance contributions to extra-budgetary funds is regulated by a separate chapter of the Tax Code of the Russian Federation. Federal Law No. 212-FZ of July 24, 2009, which regulated such payment until 2021, has become invalid. However, with regard to contributions to the Social Insurance Fund, the provisions of the Federal Law of December 29, 2006 N 255-FZ (hereinafter referred to as Federal Law No. 255-FZ) and the Federal Law of July 24, 1998 N 125-FZ (hereinafter referred to as Federal Law No. 125-FZ). Based on the totality of the provisions of the Tax Code of the Russian Federation and these laws, policyholders pay social insurance premiums. Arrears in insurance premiums to the Social Insurance Fund are the result of non-payment (late payment) of such contributions or illegally incurred expenses for the payment of insurance coverage (hereinafter - CO). Let's consider the reasons for its occurrence and the procedure for collection.

Fines, What are the consequences of late payment submission?

An insured who fails to submit a report on accidents on time will be fined under paragraph 1 of Article 26.30 of the Law of July 24, 1998 No. 125-FZ. The fine is 5 percent of the amount of contributions due to the budget for the last three months of the reporting (settlement) period. This fine will have to be paid for each full or partial month of delay. The maximum fine is 30 percent of the amount of contributions according to the calculation, and the minimum is 1000 rubles.

In addition, administrative liability is provided for late submission of calculations for insurance premiums for injuries. At the request of the FSS of Russia, the court may fine officials of the organization (for example, the manager) in the amount of 300 to 500 rubles. (Part 2).

In addition, the policyholder may be fined for refusing to provide documents that confirm the correctness of the calculation of premiums, and for missing the deadline. The fine amount is 200 rubles. for each document not submitted. The fine for the same violation for officials is 300–500 rubles. (Article 26.31 of the Law of July 24, 1998 No. 125-FZ, paragraph 3 of Article 15.33 of the Code of Administrative Offenses of the Russian Federation).

Note: If for some reason you do not agree with the decision of the territorial office of the fund, you can appeal it.

to menu

Fines for non-compliance with the established method of submitting calculations for insurance premiums

- There is a fine of 200 rubles. (Article 26.31 of the Law of July 24, 1998 No. 125-FZ). The fine for the same violation for officials is 300–500 rubles. (clause 3).

Reporting in Form 4-FSS is submitted in the prescribed form in the following ways:

- on paper ;

- electronically via telecommunications channels.

Form 4-FSS is provided to the FSS on paper, if it does not exceed 25 people. Otherwise, the reporting must be submitted electronically, certified with an electronic digital signature.

If you sent reports in Form 4-FSS via telecommunication channels, the day of its submission is considered the date of its sending.

If the electronic calculation of 4 FSS due to errors did not pass logical control, but at the same time it was transferred to the FSS in a timely manner, then officials do not have the right to hold the policyholder liable for late reporting. This conclusion was reached by the Moscow District Arbitration Court in its resolution dated 03/06/15 No. A40-109343/14.

The courts of three instances declared the fine unlawful, because Article 19 of Law No. 125-FZ provides for liability for failure to submit a report to the Social Insurance Fund within the prescribed period. And if the special communications operator confirmed that the policyholder sent the report to the payment gateway on January 25, that is, on time. And the fact that the report was submitted with erroneous calculation parameters is not evidence of a violation of the reporting deadline, since the indicated erroneous calculation parameters are not related to the reporting deadline. Since the original 4-FSS calculation was sent on time, there are no grounds for a fine.

to menu

4-FSS reporting on paper is submitted:

- personally;

Note: Passport required - through your representative;

- sent in the form of a postal item with a description of the attachment. When sending reports by mail, the day of its submission is considered the date of dispatch.

to menu

Insurance premiums according to Federal Law No. 255-FZ

Based on Part 1.1 of Article 1.1 of Federal Law No. 255-FZ, the procedure for appropriate control is regulated by the Tax Code of the Russian Federation.

From Part 6 of Article 4.7 of Federal Law No. 255-FZ, it follows that the corresponding arrears are collected by the tax authorities in the manner prescribed by the Tax Code of the Russian Federation.

Please note that tax authorities will develop collection practices starting in 2021. Currently, policyholders should pay special attention to legislation on this issue.

Organizations and entrepreneurs determine the date of accrual of such payments by the date of payment in favor of employees or other persons.

Insurance premiums must be paid monthly until the fifteenth day (inclusive) of the month that occurs after the corresponding month of payments.

Penalties for arrears in the Social Insurance Fund: features of reflection in company accounting

Late payment of contributions is grounds for the accrual of penalties. They are accrued according to the general rule for calculating bank interest from the first day of delay in making contributions to treasury accounts. Penalties for arrears are calculated as a percentage. The interest rate is determined taking into account the key rate of the Central Bank of Russia. It is recommended to transfer penalties to the Social Insurance Fund accounts simultaneously with regular contributions. Otherwise, FSS specialists will forcibly recover them from the policyholder. This tactic is established by the norms of tax law of the Russian Federation.

Late payment Accountant errors Fake sick leave certificates How much does the arrears cost in the Pension Fund and the Social Insurance Fund

Arrears in insurance premiums are actually their underpayment to the budget. Most often, it is discovered during an inspection of the Pension Fund or Social Insurance Fund. And then the company will have to recalculate insurance premiums, pay penalties and fines. Over the course of many years of practice, our experts have identified three main reasons why a company unintentionally experiences arrears in the Pension Fund of Russia and the Social Insurance Fund.

Arrears on insurance premiums (F. Law No. 255-FZ)

Arrears arise when social security contributions are not paid on time.

According to subparagraph 9 of paragraph 1 of Article 31 of the Tax Code of the Russian Federation, collection of the amount of arrears is carried out in cases established by the Tax Code of the Russian Federation. To do this, the tax authorities present (send) a corresponding demand to the policyholder.

If two months have passed since the last date of payment at the request of the tax inspectorate, and the policyholder has not paid off the arrears, the amount of which allows one to detect signs of a crime, the tax authorities will be obliged to send information about this to the relevant authorities (Article 32 of the Tax Code of the Russian Federation).

A peculiarity of arrears in social insurance contributions is that, in addition to cases of non-payment, it is formed when the territorial body of the fund does not accept the costs of paying social insurance, which the insurer carried out with the following violations:

- expenses are not supported by documents;

- the basis for the expenses are documents drawn up with errors or issued in violation of the relevant rules.

In this case, the policyholder is sent a decision not to accept expenses for offset in the prescribed form.

If a corresponding arrear arises, it will be collected by the tax inspectorate in the above order established by the Tax Code of the Russian Federation. Additionally, if there are appropriate grounds, penalties and fines may be collected.

Methods for ensuring payment of the relevant payments are specified in Article 72 of the Tax Code of the Russian Federation.

Rules for calculating the period for arrears

The date the debt was identified is the starting point for arrears. To calculate the days, the period from the identification of the debt until the formation of a demand for payment of arrears is taken. It is mandatory to set aside time to repay the debt voluntarily. Next, the days of undisputed collection are counted. If there is no money, then the mechanism of legal procedures is launched.

PLEASE NOTE: within 3 months, the FSS regulatory authority will issue an official demand for the current arrears from the moment of its discovery.

The insured debtor fulfilled the obligation to repay the debt only if the bank was represented and the latter executed a payment order to transfer funds in the required amount according to the fund details with the correct indication of arrears codes.

ATTENTION: if the payment order for arrears is filled out incorrectly, the money will go to another KBK, the debtor organization will have arrears under the Social Insurance Fund in the same amount, and penalties will continue to increase every day.

The arrears can be recognized as hopeless and written off only if there is a court decision that has entered into legal force. Otherwise, the Social Insurance Fund's demand for payment of arrears must be satisfied within 10 calendar days.