Transportation of cargo of all types by a third-party carrier is carried out in accordance with the contract and is subject to mandatory documentation. For this purpose, two forms are used: consignment note and delivery note. Both are used today, although since 2013 the TTN has been excluded from the list of mandatory documents for accounting for cargo transportation. The forms duplicate each other in many respects, but there are also differences. Is it possible to replace one form with another or should they be included in the package of transportation documents at the same time? What is the position of the regulatory authorities and how does it fit with the practice of accounting for cargo transportation?

Question: When selling furniture accessories (handles, pads, holders, etc.), the seller issued us a bill of lading and a delivery note in form N 1-T. He did not indicate the cost of the goods in the TTN. Can we accept such a TTN? View answer

Who should issue a consignment note?

If transportation of inventory items occurs directly by the owner or seller of the goods, then the execution of the document is his prerogative.

- Form and sample

- Free download

- Online viewing

- Expert tested

FILES

If an agreement with a carrier is used, which can occur both on behalf of the sender and on behalf of the recipient of the goods, then the preparation of this document may be the competence of both parties.

In other words, the 1-T form is drawn up by the company that hires the carrier.

The presumption of good faith is violated

The reasoning part of the decision of the first instance court states that the state has the right to control the conditions for the use of property or establish restrictions to ensure the payment of taxes, while preventing violations of the property rights of private individuals. Such restrictions or controls may infringe on the rights and interests of the owner. In accordance with Article

1 of Protocol 1 to the Convention for the Protection of Human Rights and Fundamental Freedoms of November 4, 1950, the principle of a balance of public and private interests must be observed.

According to this principle, no means should be chosen to achieve a public purpose that would impose undue burdens on private individuals or impose restrictions other than those that are really necessary. According to paragraph 1 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated October 12, 2006 No. 53, when resolving tax disputes, courts proceed from the presumption of good faith of taxpayers and other participants in legal relations in the economic sphere. In this regard, it is assumed that the actions of the taxpayer, resulting in the receipt of tax benefits, are economically justified, and the information contained in the tax return and financial statements is reliable. But, despite this, the courts, partially rejecting the claim, refer to the unreality and unreliability of business transactions for the purchase of goods carried out by the taxpayer and the seller.

However, the taxpayer presented all the necessary documents confirming the reality of such transactions and their economic justification: documents confirming the accrual and payment of VAT on the goods sold to the taxpayer, as well as the sale of the purchased goods and the accrual and payment of VAT on it. The inspectorate recognized that the accuracy of the information specified in the tax return and financial statements of the taxpayer is confirmed by the data of its counterparties.

There was no evidence of bad faith by the taxpayer or his counterparties, the unreality of transactions for the purchase and sale of goods and the unjustified receipt by the taxpayer of the right to a tax deduction.

Thus, there are no circumstances provided for by the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation No. 53, indicating the unfoundedness of the tax benefit and the unreality of business transactions between the seller of goods and the taxpayer. The latter was legally and justifiably required to deduct VAT in relation to the transaction of purchasing goods on the basis of a delivery note and an invoice.

Document structure

The invoice can be roughly divided into two parts.

- First - commodity, - includes information

- about the sender and recipient of the goods,

volume,

- name, etc. options.

- Second part - transport. It contains information

- directly about transportation,

information about the carrier company and the specific driver,

- car make,

- travel time and mileage,

- product, etc.

This part of the document is the basis for the decommissioning of cargo from the sender's warehouse and at the same time for its receipt by the recipient.

The cost of transportation is also indicated here.

Rules for registration and procedure for working with the form

This document refers to primary documentation, so when filling it out, you should adhere to certain standards. In particular, you must not leave cells empty (where dashes should be placed), allow inaccuracies and errors, or enter incorrect information into the form.

Additional documents may be attached to Form 1-T:

- certificates,

- passports,

- certificates,

- contracts, etc.

All of them must be indicated in the “Attachment” line of the delivery note.

The document is printed in four copies , one of which remains with the sender of the goods, the other three are handed over to the driver who will deliver the goods.

All documents must be certified with the required signatures. Then the driver must hand over the second copy to the consignee, and the third and fourth copies must be handed over to the management of the transport company (they must have the signatures of both the sender and the recipient of the goods). After this, the third copy with the issued invoice for payment for transportation services is sent to the customer (i.e., the company that entered into an agreement for the delivery of the goods), and the fourth remains with the carrier and becomes part of its accounting records.

TTN or TN?

Often accountants, managers, and workers involved in processing transportation and preparing packages of documents have questions about the advisability of using one form or another. If the use of TTN can be prescribed in the accounting policy, is it permissible to replace one document with another?

Despite the official abolition of the TTN, disputes continue to arise with fiscal authorities regarding the presence or absence of a document when registering transportation. To avoid unpleasant surprises, all three related documents are often drawn up during transportation: TTN, TN and TORG-12 consignment note, according to the principle “the more, the better.” This procedure is fixed in the accounting policy.

In what cases is a consignment note drawn up (Form N TORG-12), and in what cases is a consignment note drawn up (Form N 1-T) when shipping goods ?

Let us note a number of important points related to the use of these forms in practice.

If an organization applying VAT declares the amount to be deducted, the Federal Tax Service especially carefully checks the set of packages of primary documents, in particular the TTN. Despite Lent. Presidium of the Supreme Arbitration Court of the Russian Federation No. 8835/10 dated 09-12-2010, judicial practice to this day has not developed a unified approach on this issue. The use of a TTN confirms transportation costs and allows them to be included in amounts that reduce the income tax base.

At the same time, letter of the Ministry of Finance No. 03-03-06/1/85703 dated 12/21/17 and a number of other similar ones assert the advantage of TN in justifying transportation costs in connection with income tax calculations. It should be noted that the VAT is not separately allocated in the TTN, therefore, if there is only a TTN as a confirming document for the deduction, it will most likely be denied to the organization (Article 168 of the Tax Code of the Russian Federation).

It should be remembered that, according to Federal Law No. 259 of 08-11-07, Art. 8 (1), when concluding a contract for the carriage of goods, it is necessary to use a consignment note confirming the fact of transportation. Art. has a similar meaning. 785 of the Civil Code of the Russian Federation.

When you can’t do without TTN

According to Federal Law No. 171 of November 22, 1995 “On state regulation of the production and circulation of ethyl alcohol...”, namely Art. 10.2 (clause 1), the first among the accompanying documents for the transportation of alcohol is the TTN.

The information specified in the consignment note is confirmed by a package of other documents: certificates, declarations, certificates, but without the TTN, the transportation of alcohol by the regulatory authorities is considered illegal, as is the supply of such products itself.

A TTN is issued for each batch of alcohol, for each recipient of the goods separately, even when transported by the same transport. From the TTN data, information about the cargo enters the EGAIS (Unified State Automated Information System) system for accounting and control of alcohol circulation. Based on the TTN, declarations are generated that record “alcohol” transactions.

Attention! In the absence of a contract for the carriage of TN (and TTN) can be neglected. When exporting cargo using your own transport, you should only issue a consignment note f. TORG-12. This document can also serve as confirmation of expenses for the acquisition of medical center for NU purposes.

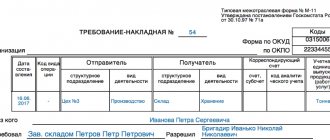

Instructions for filling out the bill of lading form

- First, you need to indicate in the document its number (according to the internal document flow of the company issuing the invoice), enter the date of completion, then in the “Shipper” line enter information about the company sending the goods - here you need to indicate its full name, actual address and telephone number.

- After this, in exactly the same way, you should enter information about the addressee in the “Consignee” line.

- Opposite the designation “Payer” you must indicate the company that pays for the carrier’s services.

- Opposite each company in the appropriate box you need to indicate its OKPO code (All-Russian Classifier of Enterprises and Organizations).

Filling out the first section of form 1-T

The first section of the invoice must be filled out almost completely by the shipper. First, detailed information about the product is entered into the table.

in the first column (but only if such an accounting system is used by the enterprise), in the second and third - the price list number and article number (also only if available). The fourth column “Quantity” must be filled in - a figure corresponding to the number of goods transported for each item separately is placed here. Columns that go further cannot be skipped either: they include -

- price per unit of goods,

- his name,

- unit of measurement (kilograms, meters, cubes, etc.),

- type of packaging (boxes, crates, barrels, bags, etc.).

Then the number of pieces, weight (in tons) and total cost for each type of product separately are entered there. If there is a markup for volume or storage or transportation costs, this should also be indicated in the table. The next step is to enter the total cost of the goods for all items and in the last column the number of the goods according to the shipper’s warehouse card is entered.

If the waybill has a continuation, then you need to note the number of additional sheets in the corresponding cell (in words) and also the total number of types of goods and places (the values are duplicated from the first table).

Next, the weight of the cargo is entered in words and figures, and after that it is necessary to indicate all available attachments (number of sheets) and below, in words, the total cost of the goods released from the warehouse.

At the bottom of the product section on the left there should be signatures with transcripts of representatives of the shipper: the person authorized to release the goods (indicating his position), the chief accountant, as well as the storekeeper who directly carried out the shipment.

On the right side, the driver’s data is entered, including information about the power of attorney that the carrier company issued for him.

Later, here below is the signature of the representative of the consignee (usually this is also a storekeeper), who, with his autograph in this part of the document, certifies the fact of acceptance of the goods after transportation safe and sound.

Grounds for review of judicial acts by way of supervision

The listed violations of substantive law by lower courts led to the emergence of the following grounds for review of judicial acts that have entered into legal force by way of supervisory review:

• decisions of lower courts violate the uniformity in the interpretation and application of the rules of law by arbitration courts (clause 1, part 1, article 304 of the Arbitration Procedure Code of the Russian Federation). In similar cases, the position of arbitration courts differs from the position of lower courts in this case (for example, Determination of the Supreme Arbitration Court of the Russian Federation dated March 19, 2008 No. 3284/08, FAS PO Resolution No. A12-9522/07 dated December 21, 2007 and FAS BVO dated March 21, 2008 No. A11-2713/2007-K2-18/162);

• incorrect application of substantive law significantly violates the rights and legitimate interests of the taxpayer in business and other economic activities and an indefinite number of persons (clause 3, part 1, article 304 of the Arbitration Procedure Code of the Russian Federation).

Clause 1 of Art. 103 of the Tax Code of the Russian Federation stipulates that when conducting a tax audit, it is not permitted to cause unlawful harm to the persons being inspected, their representatives or property in their possession, use or disposal. Due to the illegal demand of the inspectorate to reduce the VAT claimed for reimbursement from the budget on the invoice, the taxpayer was forced to bear losses in the amount of this VAT, which had already been paid to the seller when purchasing the goods. Thus, the interests of an indefinite circle of persons were violated, including the founder of the taxpayer. After all, the purpose of creating an enterprise in accordance with Art. 50 of the Civil Code of the Russian Federation is the receipt and distribution of profits between participants, and not the receipt of losses.

Thus, the courts of the first, appellate and cassation instances violated the principle of maintaining a balance of public and private interests, which resulted in the imposition of an excessive burden on the taxpayer.