on the basis of paragraph 2 of Article 169 of the Tax Code.... 2. Invoices drawn up and issued in violation of the procedure established by paragraphs 5 and 6 of this article cannot be the basis for accepting tax amounts presented to the buyer by the seller for deduction or reimbursement. Failure to comply with the requirements for the invoice, not provided for in paragraphs 5 and 6 of this article, cannot be grounds for refusal to accept for deduction the tax amounts presented by the seller. …. By putting a stamp at your discretion, you are not violating the order established by clauses 5 and 6, therefore everything is in order :) no, well, of course, there is such a position of the Ministry of Taxes, and even then they carefully write “there is no need”: .... Regarding the possibility of using additional details in invoices, the following must be taken into account. Invoices were introduced to control tax authorities over the correctness of calculation and completeness of payment of VAT to the budget by organizations and individual entrepreneurs. Resolution No. 914 establishes the necessary indicators for calculating the amount of VAT. Therefore, there is no need to use additional details in the invoice. In accordance with Article 9 of the Law of the Russian Federation of November 21, 1996 N 129-FZ “On Accounting”, the organization must document all business transactions with supporting documents, which will be primary for accounting. E. Klochkova, Moscow Department of the Ministry of Taxes and Taxes of Russia October 23, 2002 “Financial newspaper. Regional issue", N 43, October 2002.

Any transaction is accompanied by the execution of a package of documents, one of which is an invoice. Basically, VAT taxpayers issue this form. Do I need a stamp on the invoice or can I do without this detail? Let's understand the current legal requirements.

Is there a stamp on the invoice?

The basic requirements for drawing up an invoice are listed in clauses 5-6 of the stat. 169 NK. It says in detail what details the document should contain. For example, this is the serial number and date of issue; name of the parties to the transaction (seller, buyer, consignor, consignee); type of products or services sold; monetary and physical indicators of measurement; country of origin; total cost, VAT amount and rate, etc.

Additional requirements for the design of the form are contained in Decree of the Government of Russia No. 1137 dated December 26, 2011. This regulatory act contains line by line indicators that must be indicated in the invoice form. If you carefully analyze the procedure for drawing up the document, it becomes clear that affixing a seal is not required. And the absence of this requisite will not be considered a violation of legal norms.

We figured out whether or not a stamp is placed on the invoice. This document is issued without a seal, but in a standard form and in compliance with the requirements of the stat. 169 NK. Previously, the seal additionally certified the legality of the shipment, but has now been canceled. How did such an innovation affect the procedure for obtaining tax deductions for VAT?

Invoice for payment: details of its completion

How to correctly fill out an invoice to document the sale of goods (services)? The invoice form is not regulated by anyone, so the organization has the right to independently create an invoice form. The only rule is the presence in the form of the main details that are needed in order to document the facts of economic activity. To correctly fill out an invoice for payment, you must provide the following required information:

- Invoice date. This will allow the recipient to easily recognize the basis of the funds received.

- Account basis. It explains why this invoice is being issued.

- Address, telephone and fax of the seller.

- Terms of payment

- Delivery times of goods

- Information about prepayment, etc.

If the invoice was accidentally stamped

cannot be the basis for accepting those presented. tax amounts to be deducted." Therefore, having received the treasured invoice with a flaw, the accountant thinks: “Will the inspector accept such a document or not?” Let us bring clarity to all these worries. “It’s him.” “Same” It often happens that the seller ships and delivers the goods to the buyer himself.

Is VAT refundable from the budget in the following cases: - if the signatures on the invoice are made by some method of copying; - if the invoice contains surnames instead of signatures; — if the invoice does not contain columns 6 and 8 (for excise taxes) in case the products are not subject to excise taxes? Is it possible to consider the first copy (according to clause 1 of the Maintenance Procedure) of invoices issued by any method of copying, but the signatures are handwritten and there is a company seal?

For example, shortcomings and errors in the name, TIN of the buyer or seller (letter of the Ministry of Finance of the Russian Federation dated 05/02/2012 No. 03-07-11/130), incorrectly specified name of the product (letter of the Ministry of Finance of the Russian Federation dated 08/14/2015 No. 03-03-06/ 1/47252), distorted tax amount or tax rate (letter of the Federal Tax Service of Russia dated 04/11/2012 No. ED-4-3/), the use of a facsimile signature (letter of the Ministry of Finance dated 08/27/2015 No. 03-07-09/49478) - all this may pose a threat to deduction.

on the exchange of electronic invoices: sample agreement On the mutual issuance of invoices in electronic form On May 30, 2019, Romashka LLC, represented by General Director Stanislav Konstantinovich Ivanov, acting on the basis of the Charter, on the one hand, and LLC ldquo;Lutikrdquo; represented by General Director Stepankova Maria Nikitichna, acting on the basis of the Charter, on the other hand, entered into the following agreement Romashka LLC and Lyutik LLC confirms mutual agreement to issue invoices addressed to the parties to the agreement in electronic form in the format approved by order of the Federal Tax Service Russia dated March 24, 2016 No. ММВ-7-15/ The parties to the agreement confirm that they have all the technical means that allow them to accept and process electronic documents. Exchange of documents between

Quick preparation of electronic documents with signatures and seals

Of course, this does not relieve you of the need to prepare and send all the necessary documents in paper form. But you will make the originals later in a calm atmosphere. And we will help you respond quickly when you are - well, very urgently - asked to send a “copy by fax” or “scans by email”

If the invoice always has the same number of product items, then the pictures will always hit the target. In life it often turns out that this is not the case, which means that the seals and signatures on different accounts need to be moved higher or lower, preferably all together. To do this, double-click on any of the pictures. Signatures and seal (but not logo) will be highlighted with a solid frame. This means that further operations with them will occur synchronously. If you start moving one of them, the rest will “move” too. This way you can quickly drag the pictures to the desired location. But if desired, they can be moved one at a time.

Is there a stamp on the invoice?

Additional requirements for the design of the form are contained in Decree of the Government of Russia No. 1137 dated December 26, 2011. This regulatory act contains line by line indicators that must be indicated in the invoice form. If you carefully analyze the procedure for drawing up the document, it becomes clear that affixing a seal is not required. And the absence of this requisite will not be considered a violation of legal norms.

Any transaction is accompanied by the execution of a package of documents, one of which is an invoice. Basically, VAT taxpayers issue this form. Do I need a stamp on the invoice or can I do without this detail? Let's understand the current legal requirements.

When drawing up a pension certificate, is it possible to exclude months not fully worked? Home Answers to readers' questions When drawing up a pension certificate, is it possible to exclude months not fully worked? Question from Dmitry Dmitrievich Baranovsky, Astrakhan, Astrakhan Region In my younger years, I was often sick.

We figured out whether or not a stamp is placed on the invoice. This document is issued without a seal, but in a standard form and in compliance with the requirements of the stat. 169 NK. Previously, the seal additionally certified the legality of the shipment, but has now been canceled. How did such an innovation affect the procedure for obtaining tax deductions for VAT?

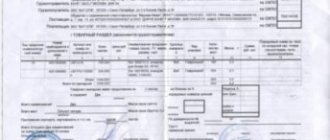

An invoice is a tax document, which is the basis for the buyer to accept the goods (works, services) presented by the seller, property rights and VAT amounts for deduction. Invoice form.

Invoices compiled and issued in violation of the order cannot be the basis for accepting VAT for deduction or reimbursement.

Invoices are drawn up when performing transactions that are recognized as an object of taxation. The invoice must indicate:

- serial number and date of issue of the invoice;

- name, address and taxpayer and buyer identification numbers;

- name and address of the shipper and consignee;

- number of the payment and settlement document in case of receiving advance or other payments for upcoming deliveries of goods (performance of work, provision of services);

- name of the goods supplied (shipped) (description of work performed, services provided) and unit of measurement (if it is possible to indicate it);

- quantity (volume) of goods (work, services) supplied (shipped) according to the invoice, based on the units of measurement adopted for it (if it is possible to indicate them);

- price (tariff) per unit of measurement (if it is possible to indicate it) under the agreement (contract) excluding tax, and in the case of applying state regulated prices (tariffs) that include tax, taking into account the amount of tax;

- the cost of goods (work, services), property rights for the entire quantity of goods supplied (shipped) according to the invoice (work performed, services rendered), transferred property rights without tax;

- the amount of excise duty on excisable goods;

- tax rate;

- the amount of tax imposed on the buyer of goods (works, services), property rights, determined based on the applicable tax rates;

- the cost of the total quantity of goods supplied (shipped) according to the invoice (work performed, services rendered), transferred property rights, taking into account the amount of tax;

- country of origin of the goods;

- Number of customs declaration.

The country of origin and the customs declaration number are indicated for goods whose country of origin is not the Russian Federation. The taxpayer selling the specified goods is responsible only for the compliance of the specified information in the invoices presented to him with the information contained in the invoices and shipping documents received by him.

The invoice is signed by the head and chief accountant of the organization or other persons authorized to do so by order or power of attorney on behalf of the organization. There is no stamp.

When issuing an invoice by an individual entrepreneur, the invoice is signed by the individual entrepreneur indicating the details of the certificate of state registration of this individual entrepreneur.

If, under the terms of the transaction, the obligation is expressed in foreign currency, then the amounts indicated in the invoice may be expressed in foreign currency.

Advertising on the website:

Advertising on the website:

All rights to the published articles belong to their authors.

direct active hyperlink to the website 2Bukh.Ru: Accounting and taxes next to

The rule that allows the VAT deduction to be applied not only in the period in which the right to it arose, but in subsequent periods, does not apply to all types of deductions.

But only on condition that the citizen being inspected himself allows them into his apartment.

Now accountants don't have to wonder about this! After all, the “vacation” series of calculators on our website has been replenished with the Vacation Experience Calculator.

The Federal Tax Service has updated the forms of documents that individuals submit to the tax office to report on their existing objects of property tax and transport tax, as well as on selected real estate objects in respect of which a benefit is provided.

It is planned to amend the accounting law, according to which organizations will no longer have to submit annual accounting (financial) statements to both the tax office and “statistics”. True, at the same time the opportunity to submit accounting reports on paper will disappear.

If a traveler's air ticket was purchased electronically, a security-stamped boarding pass is required, among other things, to verify travel expenses for "revenue" purposes. But what to do if it is not customary to put such marks at a foreign airport?

According to the Tax Code, one of the parents can refuse the standard personal income tax deduction for a child in favor of the second parent, so that he can receive a double personal income tax deduction. True, it is not entirely clear what this double deduction will be if the number of children of each parent of a common child is different.

>TYPICAL SITUATION 199839

Printing on invoices

A businessman who last issued an invoice a decade and a half ago may today wonder whether it is necessary to put a stamp, because in the past, a seal was a mandatory requirement for this document. Without her presence, drawing up an invoice was meaningless, and tax deductions were impossible. In those days, the status of any document without a seal was insignificant.

Modern requirements for stamping documents have changed radically. For example, now companies are allowed not to have a seal at all, if it is not mentioned in their charter. This became possible from 04/07/2015 (clause 7, article 2 of the Law of December 26, 1995 No. 208-FZ “On Joint-Stock Companies”, clause 5 of Article 2 of the Law of 02/08/1998 No. 14-FZ “On Limited Liability Companies” ").

Thus, printing on an invoice has not been a mandatory requirement for many years. Although those who are not yet accustomed to documents without a seal can put it as an additional detail (letter of the Ministry of Finance dated October 30, 2012 No. 03-07-09/146, Federal Tax Service dated January 26, 2012 No. ED-4-3/1193).

Even if a businessman, out of habit, stamped the invoice, the fate of the tax deduction will not change. First of all, you need to pay attention to the completeness and correctness of the required details, because otherwise problems with deductions cannot be avoided. For example, shortcomings and errors in the name, TIN of the buyer or seller (letter of the Ministry of Finance of the Russian Federation dated 05/02/2012 No. 03-07-11/130), incorrectly specified name of the product (letter of the Ministry of Finance of the Russian Federation dated 08/14/2015 No. 03-03-06/ 1/47252), distorted tax amount or tax rate (letter of the Federal Tax Service of Russia dated April 11, 2012 No. ED-4-3 / [email protected] ), use of a facsimile signature (letter of the Ministry of Finance dated August 27, 2015 No. 03-07-09/49478 ) - all this can become a threat to deduction.

Enter the site

The details required for the primary accounting document are listed in the Law of the Republic of Belarus “On Accounting and Reporting” dated October 18, 1994 No. 3321 – XII (as amended on May 17, 2021). By the way, this Law defines primary accounting documents as a document that confirms the fact of any business transaction (Part 1, Article 9). A business transaction is interpreted broadly by law and is defined as “an action or event that entails changes in the volume and (or) composition of the property and (or) obligations of the organization” (Part 13 of Article 2 of the Law). The law does not include a seal imprint among the required details. HOWEVER, there is no need to rush. Regarding the preparation of certain types of primary accounting documents, special regulations of direct effect have been adopted. Almost every one there states that the primary document is certified by a seal. Please note - If errors or inaccuracies are found in the completed invoice, it is allowed to make corrections in a way that does not interfere with the reading of the previous entry, with the obligatory affixing of the date and signature of the person who made the corrections, and certification of the corrections made with a seal (CLARIFICATION of the Ministry of Finance of the Republic of Belarus dated July 15, 2021 No. 15-9/338 “On the procedure for using goods, transport and delivery notes”).

We recommend reading: Age of a minor

Minutes of general meetings of participants, decisions of owners of unitary enterprises. Neither the Law of the Republic of Belarus dated December 9, 1992 No. 2021-XII (as amended on July 30, 2021) “On joint stock companies, limited liability companies and additional liability companies”, nor the Law of the Republic of Belarus “On Business Companies” that has not yet entered into force (effective from 02.08.2021) do not contain a direct indication of the mandatory presence of a seal on these documents, with the exception of ballots for absentee voting.

Latest publications

The Ministry of Finance of Russia clarified that if an agent on the simplified tax system acts in the interests of the principal, then in a transaction with third parties, only agency fees are taken into account as part of his income when determining the object of taxation (letter of the Department of Tax and Customs Policy of the Ministry of Finance of Russia dated September 28, 2021 No. 03 -11-06/2/62942).

When planning the opening of a new store, the manager usually asks the question: do I need to report this to the Federal Tax Service? A trading company must be registered as a UTII payer with the inspectorate at the place of business in each municipality where it intends to report under this special regime.

Currently, the professional standard “Accountant” is in force. However, in the near future, the Russian Ministry of Labor plans to adjust the requirements for the qualification level of accounting workers, as well as clarify their labor functions. For this purpose, a draft of a new professional standard “Accountant” has already been prepared.

The Saratov Regional Duma adopted a law on the transition to a new procedure for determining property tax for individuals. From January 1, 2018, payments will be calculated not according to the inventory value, but according to the cadastral value. Saratov residents will have to pay the newly assessed tax in 2021.

In the article we will look at how to correctly reflect in the accounting and tax accounting of budgetary and autonomous institutions the surpluses and shortages of property identified during the inventory, in what order to write off unrecoverable receivables and unclaimed accounts payable, and what documents to formalize these transactions.